LC vs SBLC: What Is the Difference?

A practical business guide explaining the difference between a Letter of Credit and a Standby Letter of Credit, including purpose, payment trigger, use cases, risks, and when each instrument is suitable.

Contents

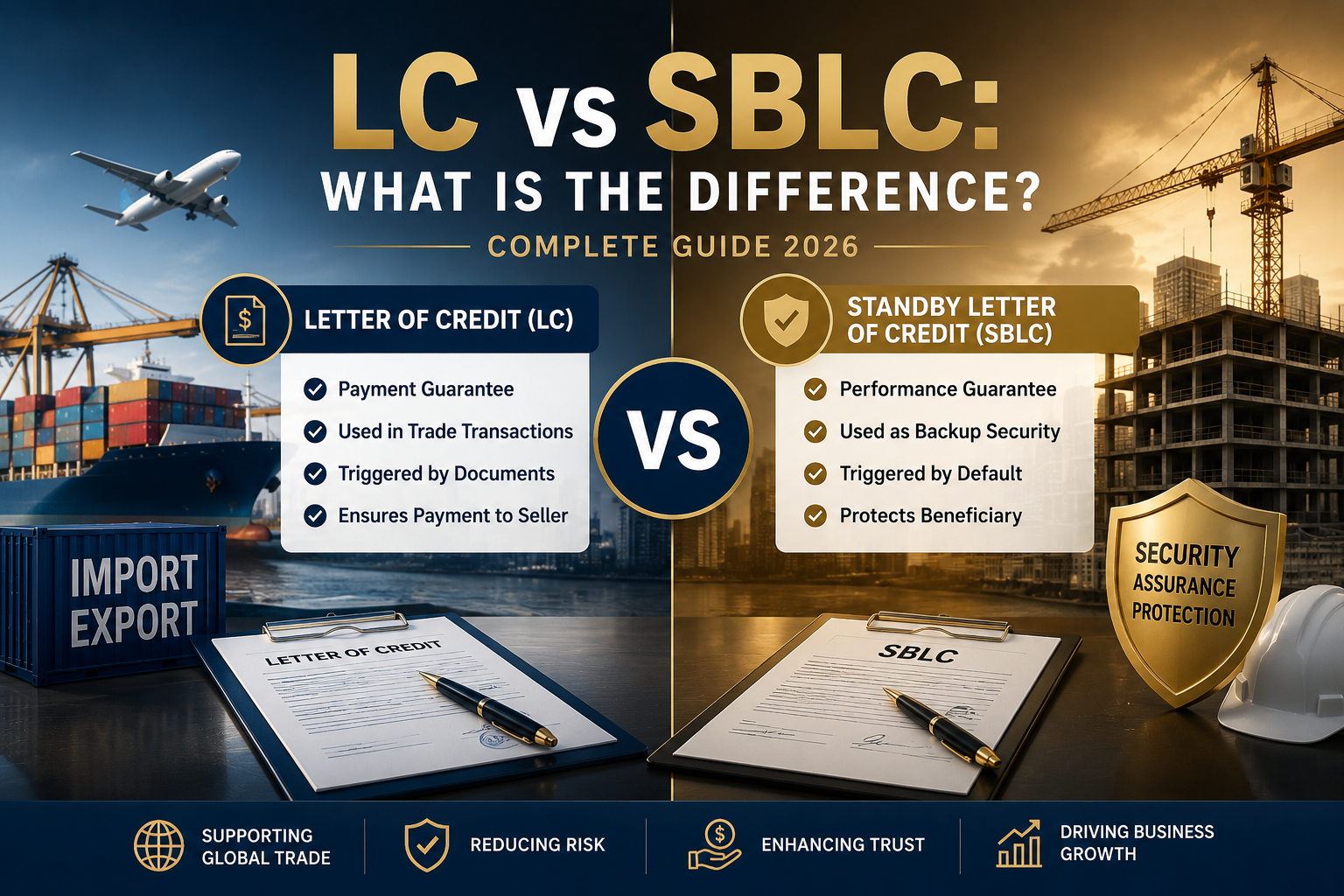

A Letter of Credit (LC) and a Standby Letter of Credit (SBLC) are both bank instruments used to reduce financial risk, but they are not the same. An LC is mainly used as a payment mechanism in trade, while an SBLC works as backup security if a party fails to perform or pay.

Understanding the difference between LC and SBLC is important for importers, exporters, contractors, suppliers, traders, and businesses involved in domestic or international transactions.

What Is a Letter of Credit (LC)?

A Letter of Credit is a bank-issued payment undertaking used mainly in trade transactions. It gives the seller confidence that payment will be made when the required documents and agreed conditions are fulfilled.

In simple terms, the buyer’s bank promises to pay the seller after the seller ships the goods and presents compliant documents. The LC helps both parties complete the transaction with more confidence.

An LC is normally used to pay the seller in a trade transaction, provided the seller meets the documentary requirements.

What Is an SBLC?

A Standby Letter of Credit is a bank-issued guarantee used as backup protection. It is usually not intended to be drawn under normal circumstances. It becomes useful if the applicant fails to pay, perform, or meet the agreed obligation.

In simple terms, the buyer or applicant is expected to fulfill the contract normally. If they fail, the beneficiary may claim under the SBLC according to its terms.

An SBLC is a financial safety net. It protects the beneficiary if the applicant defaults or fails to perform.

Main Difference Between LC and SBLC

The main difference is purpose. An LC is designed to support payment in a trade transaction. An SBLC is designed to provide backup assurance if something goes wrong.

| Feature | Letter of Credit (LC) | Standby Letter of Credit (SBLC) |

|---|---|---|

| Primary Purpose | Payment mechanism for trade transactions | Backup guarantee if the applicant defaults |

| When Payment Happens | When compliant documents are presented | When the applicant fails to pay or perform |

| Common Use | Import and export of goods | Contracts, performance security, financial assurance |

| Expected Usage | Usually expected to be used for payment | Ideally not used unless default occurs |

| Best For | Shipment-based trade transactions | Large contracts, project obligations, backup protection |

| Nature | Trade payment instrument | Guarantee or security instrument |

Need help choosing between LC and SBLC?

Share your transaction type, amount, timeline, buyer or beneficiary details, and required instrument so the structure can be reviewed properly.

How a Letter of Credit Works

An LC follows a document-based process. The bank checks the documents against the LC terms before payment is released.

How an SBLC Works

An SBLC works as backup security. It is usually claimed only if the applicant does not meet the obligation under the contract.

Types of Letter of Credit

Common LC structures include:

- Sight LC

- Usance LC

- Confirmed LC

- Revolving LC

- Transferable LC

- Back-to-Back LC

Types of SBLC

Common SBLC structures include:

- Financial SBLC

- Performance SBLC

- Direct Pay SBLC

- Advance Payment SBLC

- Bid Bond SBLC

When Should a Business Use LC?

A business usually uses an LC when the transaction involves shipment of goods and the seller wants payment assurance before releasing goods or documents.

- Importing goods from overseas suppliers

- Exporting products to new buyers

- Managing trade with unfamiliar counterparties

- Reducing payment risk in cross-border trade

- Supporting supplier confidence in large orders

When Should a Business Use SBLC?

A business usually uses an SBLC when the beneficiary wants assurance that payment or performance will be backed by a bank if the applicant fails to meet the obligation.

- Securing large contracts

- Providing performance assurance

- Supporting infrastructure or construction projects

- Backing payment obligations

- Improving credibility with counterparties

Advantages of LC

- Supports secure trade payment

- Reduces seller payment risk

- Gives buyers and sellers a clear document-based structure

- Widely accepted in international trade

- Helps build supplier confidence

Advantages of SBLC

- Provides backup financial protection

- Improves business credibility

- Supports large-value contracts and obligations

- Can protect against default or non-performance

- Useful in commercial, financial, and project-based transactions

Risks and Challenges

Both LC and SBLC require proper documentation, clear terms, and careful banking review. Mistakes in wording, conditions, expiry dates, documents, or claim requirements can create delays or disputes.

| Instrument | Common Risks | How to Reduce Risk |

|---|---|---|

| LC | Document discrepancies, delayed shipment, unclear payment terms, bank compliance issues | Review LC wording, prepare documents correctly, confirm shipment timelines, align invoice and transport documents |

| SBLC | Improper claim wording, expiry issues, fraud risk, high issuance cost, unclear default conditions | Use clear terms, define claim documents, check beneficiary requirements, review expiry and governing rules |

LC vs SBLC: Which Is Better?

Neither instrument is automatically better. The right choice depends on the transaction. If the main purpose is trade payment against documents, an LC is usually more suitable. If the main purpose is backup assurance against default or non-performance, an SBLC is usually more suitable.

Use LC when the seller needs payment through a trade document process. Use SBLC when the beneficiary needs security if the applicant fails to pay or perform.

Can LC and SBLC Be Used Together?

Yes. In complex transactions, LC and SBLC can sometimes be used together. For example, an LC may support the payment flow, while an SBLC provides additional security for performance, repayment, or contract assurance.

Key Documents for LC and SBLC

Common documents may include:

- Commercial invoice

- Purchase order or contract agreement

- Bill of lading or airway bill

- Packing list

- Insurance certificate

- Certificate of origin

- Beneficiary details

- Claim documents for SBLC

International Rules for LC and SBLC

LCs are commonly issued subject to UCP 600 rules. SBLCs are commonly issued subject to ISP98 or sometimes UCP 600, depending on the transaction and bank requirements.

Conclusion

An LC and an SBLC are both valuable trade finance instruments, but they solve different problems. An LC supports payment in a trade transaction, while an SBLC provides backup protection if a party fails to meet its obligation.

For businesses involved in import, export, contracting, commodities, infrastructure, or structured finance transactions, choosing the right instrument can reduce risk, improve trust, and help the transaction move forward with stronger financial confidence.

Reviewed by National Finance Insights

National Finance publishes practical finance guides for businesses covering trade finance, Letters of Credit, SBLC, Bank Guarantees, corporate funding, structured finance, and transaction readiness.

LC vs SBLC FAQs

Common questions businesses ask when comparing Letters of Credit and Standby Letters of Credit.

Is an LC the same as an SBLC?

No. An LC is mainly used as a payment instrument in trade transactions, while an SBLC is usually used as backup security if the applicant defaults or fails to perform.

Which is better, LC or SBLC?

Neither is always better. An LC is more suitable for shipment-based trade payments. An SBLC is more suitable for backup assurance, contract security, and default protection.

When is payment made under an LC?

Payment is usually made when the seller presents documents that comply with the LC terms, such as invoice, bill of lading, packing list, and other required documents.

When is an SBLC claimed?

An SBLC is usually claimed when the applicant fails to pay, perform, or fulfill an agreed obligation, subject to the claim conditions stated in the SBLC.

Can LC and SBLC be used for international trade?

Yes. Both instruments are commonly used in international business, but LC is more directly connected to trade payment, while SBLC is more connected to backup security.

Related finance topics

Continue reading practical guides connected to trade finance, banking instruments, and structured finance.

Need LC or SBLC support for your transaction?

If your business is handling an active requirement involving LC, SBLC, trade finance, bank guarantees, supplier payment, import, export, or contract security, National Finance can review the structure and guide the next step.